An excerpt from the GTA Member Webinar on November 15, 2025.

Transcript edited for print.

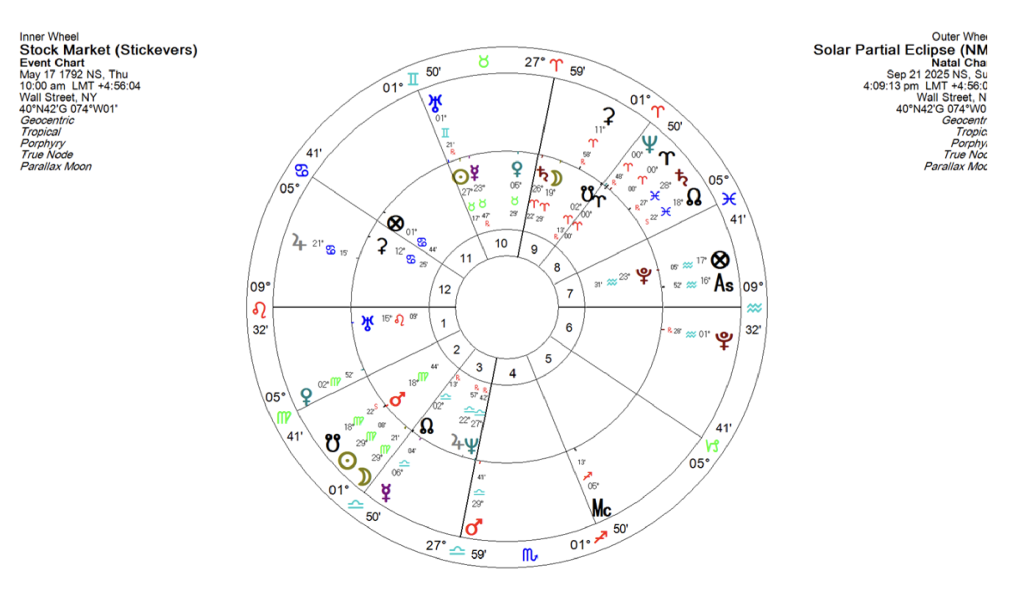

The September eclipse (2025) was very important. What we noted was that it hit the second house of the U.S. chart.

And we know the second house has to do with wealth, money, the monetary base, banking resources, the banks themselves, and capital formation. It deals with the banking system, credit expansion, and overall money supply—M0, M1, M2, M3. It also ties into central bank policy, commodity reserves, tax flows—basically any type of asset that can be taxed and shows up on the general ledger.

So this is really the nation’s financial foundation.

Now, when you see an eclipse—this one is opposing Saturn and Neptune in the eighth house. And the eighth house deals with taxation, debt, bankruptcies, and lending. Not just personal loans, but bank-to-bank lending, institutional loans, and even nations lending to other nations.

So what we’re seeing is this eclipse activating both houses at the same time.

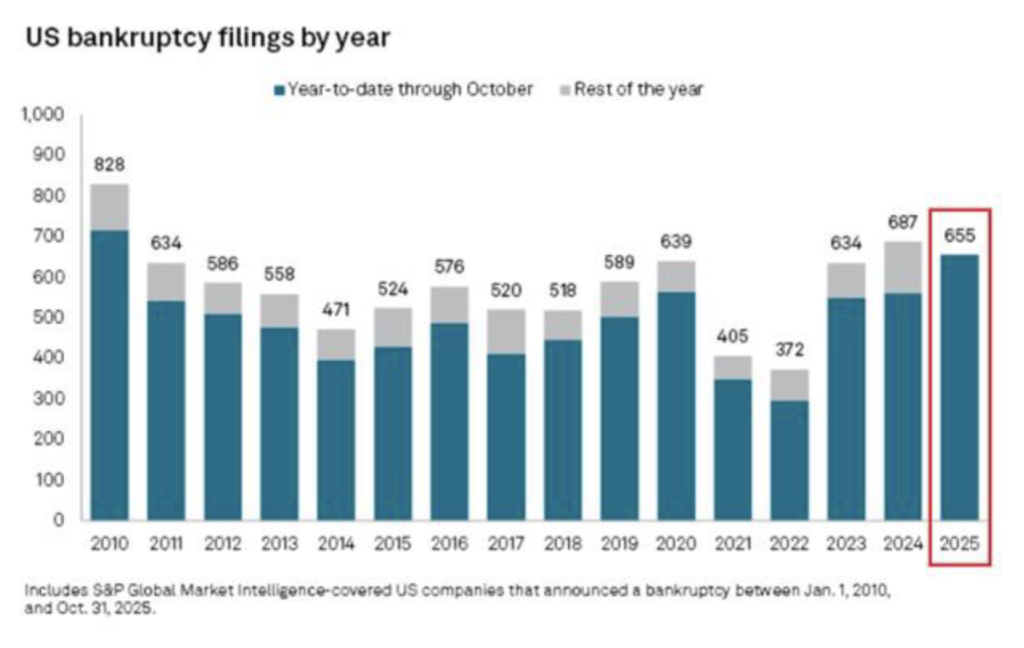

Rising Bankruptcies Signal Systemic Stress

And what do we see in reality? Year-to-date, 655 large U.S. companies have gone bankrupt—the highest number in 15 years. And we’re not even done with the year. We’re approaching 2010 levels, and if you remember, that was during the Great Recession.

Since 2022, bankruptcies have risen nearly 100%. That’s even greater than during the COVID crisis. Back in 2021–2022, we had COVID, but now we’re seeing even worse numbers.

Corporate bankruptcies are running at a crisis pace. And it’s not just smaller companies—these include large firms. In 2008, those companies got bailed out. During COVID, they got bailed out. This time, they’re not.

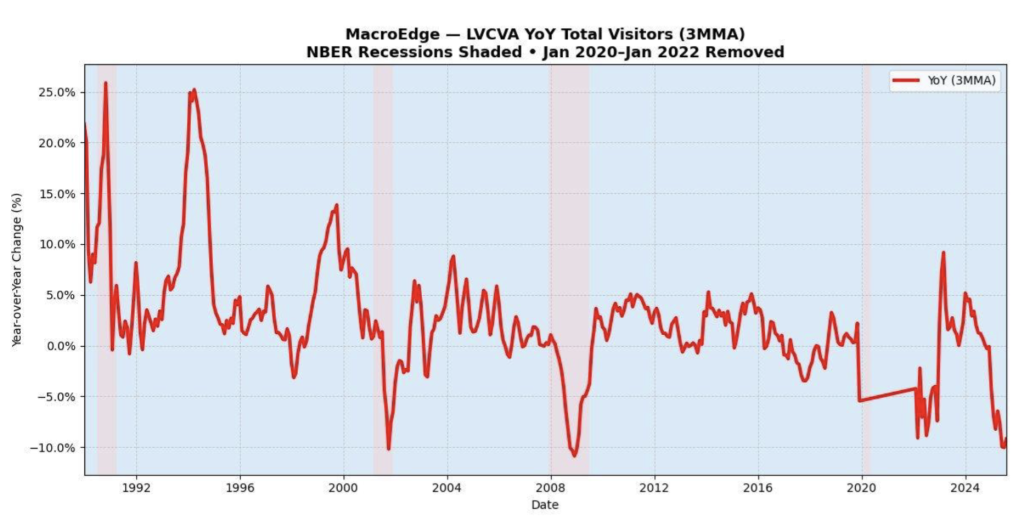

The Real Economy Is Already Slowing

Now look at what’s happening in the real economy. Total visitor count to Las Vegas is down another 9% in 2025. If you compare that to 2008, when casinos were closing, we’re starting to see a similar pattern. And it keeps dropping.

This is the sharpest collapse since the 2008 crash. The Strip economy is bleeding while tables sit empty. This isn’t just tourist fatigue—it’s the erosion of discretionary spending.

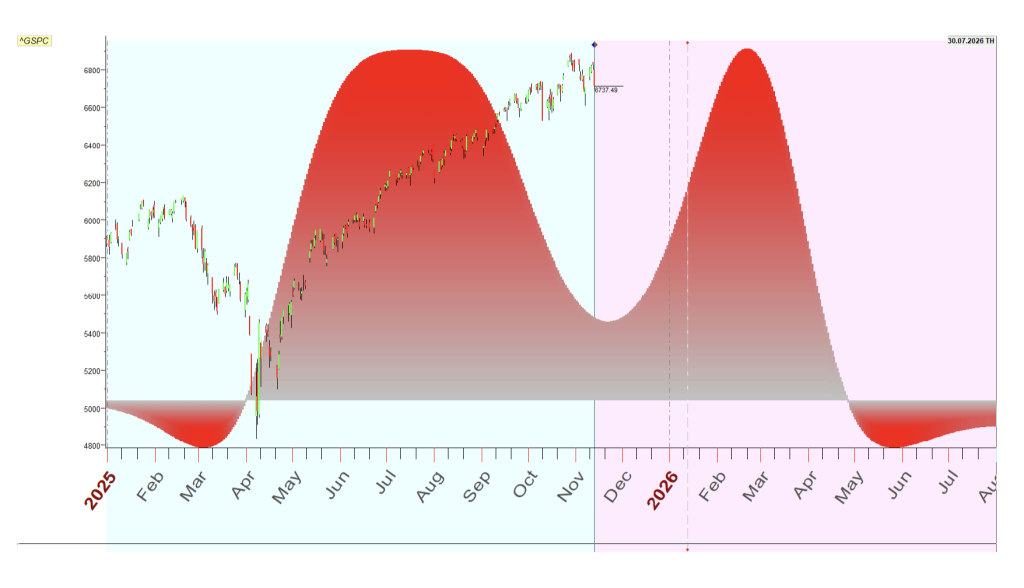

The “Big Beautiful Bubble” and Market Contradictions

At the same time, what do we see? The so-called “big beautiful bubble.” After the “big beautiful bill” was passed, the stock market just kept going up higher and higher.

And what’s powering that? The Saturn-Neptune alignment.

If you look at the chart, the red line represents that alignment. Notice when the bubble peaks—it peaks in February.

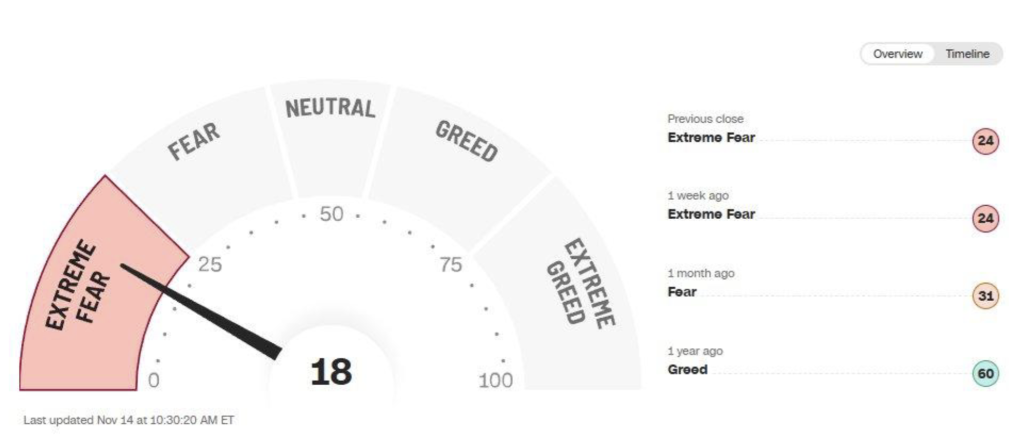

So what does this tell us? Liquidity is king. But here’s the contradiction: while the stock market is going up, there’s extreme fear in the market. And that’s not what you typically see before a crash.

For example, the S&P is trading just 2% away from its all-time high—basically at record levels. But at the same time, there’s extreme fear.

Warning Signals Are Emerging Across the System

Then we start seeing signals. Slowly at first, then all at once.

- Warren Buffett says he’ll no longer write the Berkshire annual letter.

- Michael Burry—Mr. Big Short—announces he’s closing his fund.

- The White House says last month’s job report will never be released.

- The yield curve finally un-inverts after a record stretch—that’s a classic recession signal.

- Luxury home sales fall at the fastest pace since the financial crisis.

- Corporate bankruptcies hit their highest monthly level since 2009.

So what is all of this telling us? A liquidity crisis has already begun.

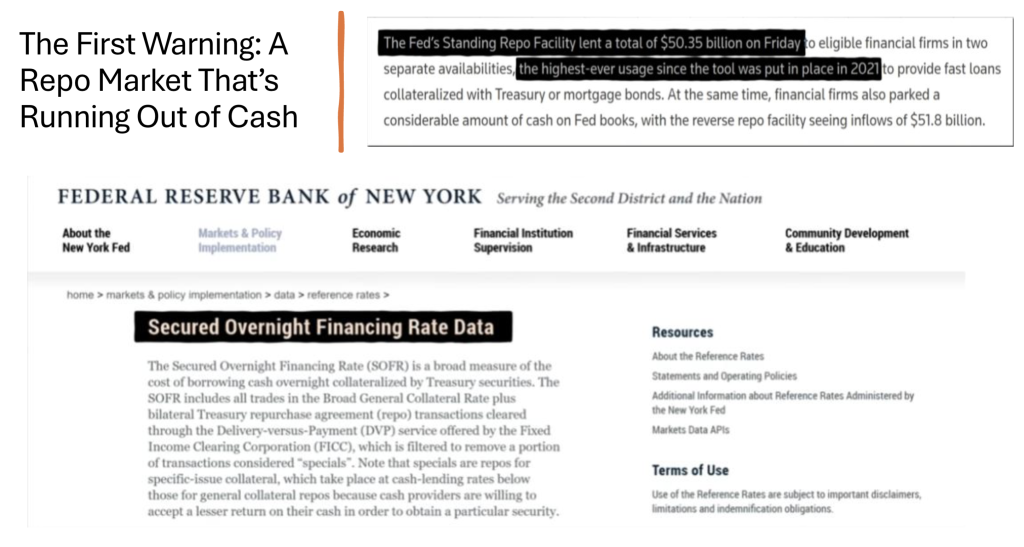

The Repo Market: Hidden Stress in the Financial System

There’s a major problem with liquidity in the system. And the first warning sign was the repo market running out of cash.

The Fed created the standing repo facility in 2021 to prevent funding freezes. Only about 40 large banks can access it, and there’s a stigma to using it—it signals weakness.

For nearly two years, usage was near zero. Then on October 31st, banks suddenly borrowed $50 billion from it—the highest usage since the program launched. And this is happening with no headline crisis. No pandemic. No failed treasury auction.

Banks are choosing embarrassment over illiquidity. That tells you something is deeply wrong.

The repo market is basically the circulation system of the financial world. Banks, dealers, and money funds borrow and lend cash overnight against treasury collateral. And when the repo market starts to seize up, the whole system is at risk.

We saw this in 2008 with Lehman. We saw it again in March 2020 during the pandemic. And now the same warning signs are flashing again.

Liquidity Is Drying Up Internally

Even though global liquidity is increasing, internal liquidity in the U.S. is drying up. We’re approaching crisis levels.

You can see it in reports—U.S. bank reserves have dropped to $2.8 trillion, a four-year low. Analysts are warning a crisis could be near.

So there’s a quiet, hidden stress building in the system. It’s not showing up yet in bank failures or market crashes, but it’s underneath—in the plumbing of the system, the repo market.

Signals from this massive ecosystem suggest the Fed is losing bank reserves—cash held at the Fed—which is the raw material for lending.

The key point is this: the Fed has been draining liquidity through quantitative tightening.

When Biden became president, policy shifted from QE to QT. Since then, reserves have fallen sharply—from peak levels down to $2.8 trillion. And that matters, because reserves act like shock absorbers for the financial system. When they shrink, markets become unstable. Rates get volatile. The system starts to strain.

Since June 2022, the Fed has drained $2.4 trillion in liquidity. Repo rates are now jumping. Facilities across the system are being tapped. And reserves are just barely above the minimum safe level.

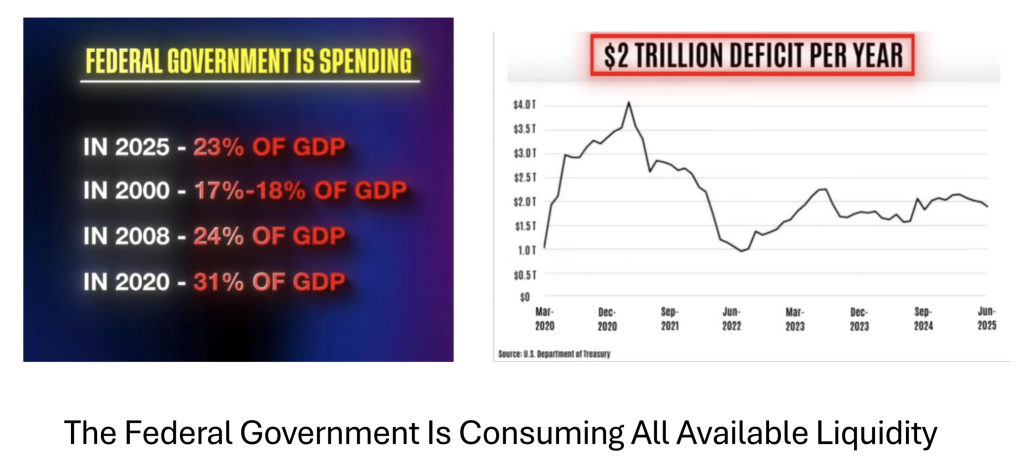

Government Spending and the Liquidity Strain

So what’s the core problem? Government spending. Right now, federal spending is about 23% of GDP. And they’re not generating enough income to support that—they’re printing money to cover it.

Total federal debt is around $38 trillion—basically 100% of GDP. Almost everything the country produces is going toward servicing that debt.

The annual deficit is over $2 trillion every year. And spending is higher than during 2008. Higher than World War II. Higher than any crisis.

At the same time, the Treasury is flooding the market with new bonds. Banks and funds buy them, but they finance those purchases through the repo market.

So the government is draining liquidity faster than the Fed can replace it. And neither political party is willing to cut spending because if they do, they won’t get reelected.

Even when it comes to major structural drivers of the deficit—like Social Security—nothing is seriously on the table. And that’s a key point, because addressing programs like that could potentially resolve a significant portion of the problem. But politically, it’s untouchable.

The Inevitable Outcome: More Money Printing

So what happens instead? They keep printing more money.

In 2021, they expanded the money supply by 31%. In 2008, it was about 24%. And they’ll keep doing it.

Because cutting spending isn’t on the table—for Social Security, Medicare, defense—none of it. Both parties will continue spending. And that’s what’s driving this growing demand—and strain—on liquidity in the system.

To watch the full presentation and more like this, join the Global Transformation Astrology Membership. Go to gta.williamstickevers.com and become a GTA member today.

A trends forecaster, William’s annual global forecasts are backed by a deep study of economies, geopolitics, archetypal cosmology, and modern astrological forecasting techniques. William’s predictions for the outcome of the U.S. Midterm and Presidential Elections are well documented on his blog.

William Stickevers is a strategic astrological advisor, advising clients from 28 countries for nearly four decades with strategy and cosmic insight and foresight to gain an asymmetrical advantage in their investing, business planning and decisions, and to live a more fulfilled life according to their soul’s code and calling.

William has been a regular guest on Coast to Coast AM with George Noory and The Jerry Wills Show, and featured on The Unexplained with Howard Hughes, Beyond Reality Radio with Jason Hawes and JV Johnson, We Don’t Die Radio with Sandra Champlain, Supernatural Girlz, Paranormal Podcast, and Alan Steinfeld’s New Realities. An international speaker, William has lectured at the New York Open Center, Edgar Cayce’s Association for Research and Enlightenment (A.R.E.), two Funai Media events in Tokyo, Japan, the United Astrology Conference (2018), for the National Council for Geocosmic Research (NYC, Long Island, New Jersey, San Francisco chapters), American Federation of Astrologers (Los Angeles), the Astrological Society of Connecticut, the San Francisco Astrological Society, and in Europe (Munich and Bucharest) and Japan (Tokyo, Osaka, Yokohama).

More information on Programs, Consultations and Forecast Webinars are at his website www.williamstickevers.com.